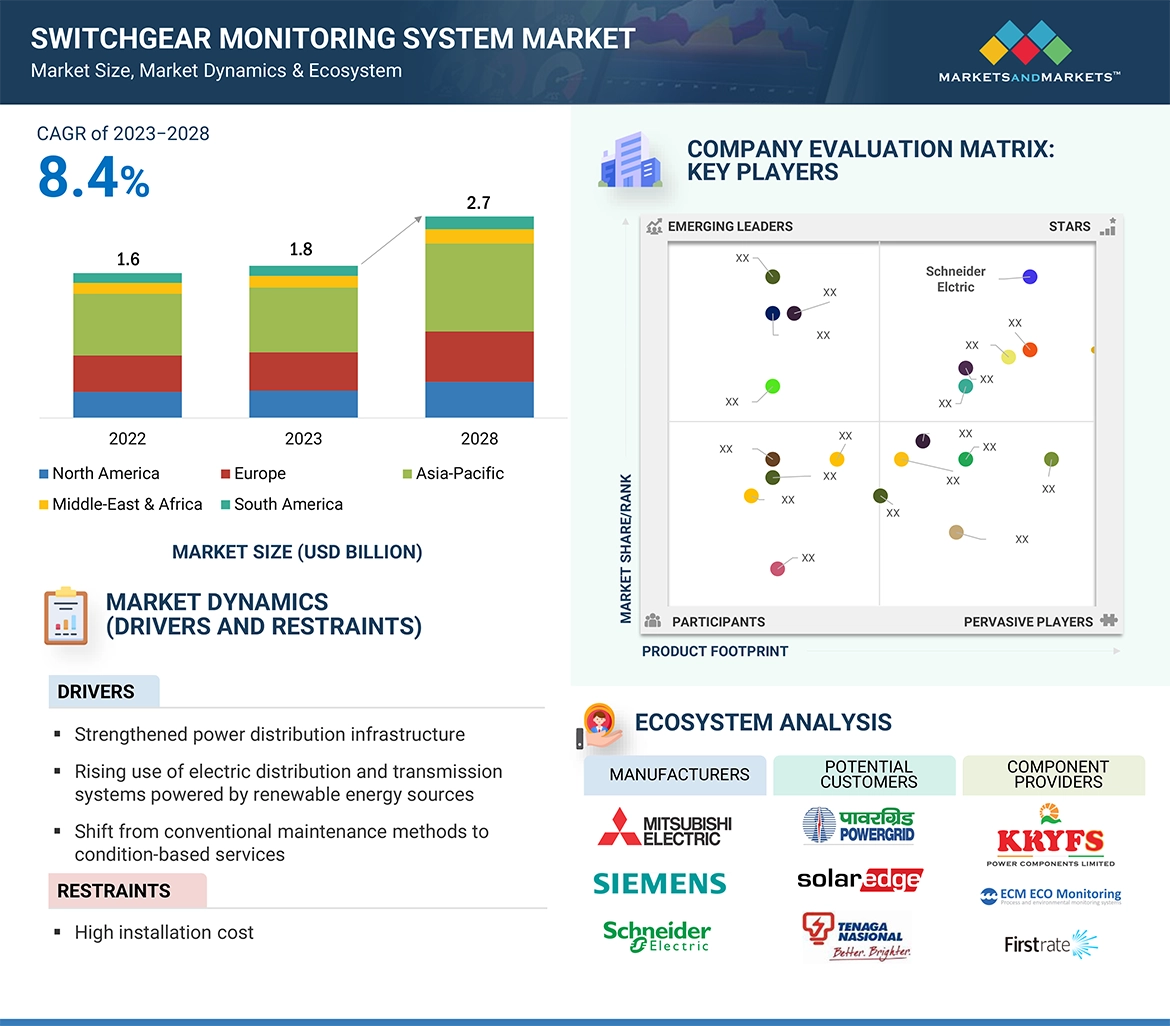

The global Switchgear Monitoring System Market is projected to reach USD 2.7 billion by 2028 from an estimated USD 1.8 billion in 2023, at a CAGR of 8.4% during the forecast period. The demand to secure electrical distribution systems is the need for the continuous monitoring of switchgear, and growing investments in renewable energy offer high-growth opportunities for the market.

Gas Insulated Switchgear, by type, is expected to grow by the largest segment during the forecast period.

Based on type, the switchgear monitoring system market has been segmented into gas insulated switchgear and air insulated switchgear. Monitoring systems are in high demand for the Gas insulated switchgear systems, as switchgear monitoring systems are essential for gas-insulated switchgear (GIS) to ensure its reliability, safety, and longevity. GIS is a type of high-voltage switchgear that uses sulfur hexafluoride (SF6) gas as an insulating medium. SF6 gas is a highly effective insulator, but it can also pose environmental hazards if it leaks. Therefore, it is important to monitor the SF6 gas pressure and density in GIS to ensure that it is not leaking.

In North America, the adoption of GIS monitoring systems is expected to rise due to increasing investments in grid modernization and renewable energy integration. Utilities across the region are prioritizing advanced monitoring technologies to improve operational efficiency and comply with stringent environmental regulations regarding SF6 gas emissions.Additionally, growing demand for reliable power infrastructure in urban areas, along with the replacement of aging grid components, is driving the need for GIS monitoring solutions in North America.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=69776366

The partial discharge monitoring segment, by services segment, is expected to grow at the second fastest CAGR during the forecast period.

This report segments the switchgear monitoring system market based on services into partial discharge monitoring, gas monitoring, temperature monitoring, and others. Partial discharge within switchgear poses a significant risk as it can lead to insulation breakdown, resulting in critical issues like electrical arcing and equipment failure. The implementation of partial discharge monitoring not only enhances operator safety but also instills confidence in the reliability and safety of electrical equipment.

In North America, the demand for partial discharge monitoring systems is expected to rise due to the region’s focus on grid modernization, increasing adoption of smart grid technologies, and stringent regulatory standards for electrical safety. Utilities and industrial operators are investing in predictive maintenance solutions to minimize downtime and optimize the lifespan of switchgear assets. Additionally, with aging power infrastructure in the US and Canada, there is a growing need for advanced monitoring solutions to prevent equipment failures and ensure uninterrupted power supply.

Software is expected to be the fastest segment, by component in the switchgear monitoring system market.

This report segments the switchgear monitoring system market based on component into Hardware and software. The pivotal role of hardware in establishing a robust switchgear monitoring platform cannot be overstated. Hardware devices play a crucial role in overseeing, measuring, transmitting, and analyzing data across various sectors, including process and non-process industries, utilities, the commercial sector, and beyond. The continuous innovation in hardware solutions is expected to further enhance the reliability, intelligence, and adaptability of these systems across a wide range of industrial and commercial applications.

In North America, the rapid adoption of software-driven switchgear monitoring solutions is being fueled by the increasing need for real-time data analytics, predictive maintenance, and grid reliability enhancements. With utilities and industrial sectors shifting towards digitalization, cloud-based monitoring platforms and AI-powered analytics are gaining traction to optimize asset performance and reduce operational risks. Furthermore, the integration of software with IoT-enabled switchgear is driving the demand for advanced monitoring systems, particularly in the US and Canada, where smart grid initiatives and regulatory compliance measures are accelerating the transition to intelligent switchgear solutions.

Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=69776366

North America is expected to be the second fastest region in the switchgear monitoring system market.

The US government has set a target to reduce carbon pollution from the power sector by 32% below the 2005 levels by 2030. To achieve this, utilities in the US and Canada plan to replace and upgrade aging power infrastructure, improving reliability and power generation capacity. According to the DOE, power blackouts are costing USD 150 billion per year in North America. Most of the power infrastructure, which is unreliable, poses a threat to national security. These factors positively push the North American power distribution sector, creating growth opportunities for the switchgear monitoring system markets.

Key Players

Some of the major players in the Switchgear Monitoring System market are ABB (Switzerland), Siemens Energy (Germany), Schneider Electric (France), General Electric (US), and Eaton (Ireland).